Q4 2025 Market Commentary

The fourth quarter’s start coincided with the beginning of the longest government shutdown in US history. Despite this, stocks gained 2.4% during the 43-day government closure, setting record highs by mid-November.

The market had a mid-quarter tantrum, falling 5% in eight days, as concerns over tech valuations, combined with inflation fears and worries of a hawkish Fed, weighed on markets. The decline was short-lived. The Federal Reserve still cut rates in December, and US stocks regained lost ground, finishing the quarter up 2.5%.

Price Action

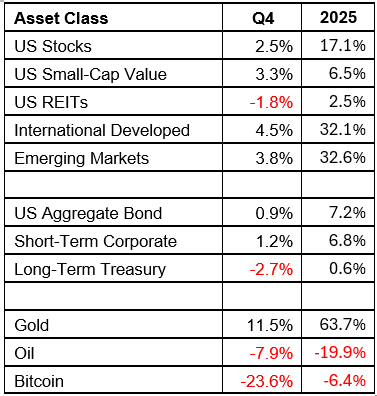

In many ways, the 4th quarter was representative of 2025. International stocks were the best-performing equity asset class, Real Estate Investment Trusts (REITs) were the worst, gold showed the strongest returns of any major investment, the treasury curve steepened, and Bitcoin did poorly.

International equities were the star of 2025, gaining 32%, far outpacing US Stocks 17%. The historical return premium of small-cap value stocks showed up in a big way in international stocks, with those funds up an eye-popping 49%. Interestingly, small-cap value companies in the US did not reciprocate, gaining 7% for the year and underperforming domestic large-caps.

With the treasury curve steepening, short and intermediate-term bonds had strong returns while very long-term bonds declined due to rising interest rates in the back-end of the curve.

- US stocks posted a solid quarter and another strong year. (Up 2.5% and 17.1% respectively).

- International stocks were the best-performing equity in the quarter and in 2025 (Up 4.5% and 32.4% respectively).

- Long-dated treasuries fell in Q4 (-2.6%) and finished the year close to flat (+0.6%).

- REITs lost 1.8% in Q4 finishing the year up only 2.5%.

- Gold gained 11.5% in the fourth quarter, finishing the year up 63.7% - its best showing since the 1970s!

- Speculators in Bitcoin were frustrated in Q4 (-23.6%), which turned 2025 negative (-6.4%).

- The housing market softened, dropping 0.8% for the last three months we have data.

Looking Forward

The Federal Reserve cut rates four times in 2024, three times in 2025, and is expected to cut only twice in 2026. With the Fed’s actions expected to be more muted next year, look to corporate earnings and inflation as primary drivers of returns in 2026.

Markets tend to revert to their mean over time. In 2025, International stocks regained much of the ground they had lost to US stocks over the last decade. Still on deck are domestic small-caps and REITs. While US large growth stocks are trading 45% above historical earnings valuations, small-caps are only 4% above their historical p/e. Meanwhile, US REITs are trading at a 4% discount, just about the only equity asset class in the world not trading at a historical premium.

As always, the most significant force in the market will be something we can’t predict, news that has yet to happen. At the time of this writing, the U.S. just captured Venezuela’s president, Nicolas Maduro. Meanwhile, some believe gold’s historic year was driven by concerns behind the US national debt – a slow-moving, yet potentially devastating macroeconomic condition that Congress (and voters) seem unwilling to address. Despite these headwinds, human ingenuity has always carried the day and may yet again, with the emergence of Artificial Intelligence. What the future holds is anyone’s guess, but we do know that disciplined and diversified investing has always done well in the long-run and there is little reason to think that will change.