Q2 2025 Market Commentary

Market Commentary

The quarter began with a bang as President Trump’s announcement of tariff increases sent markets sharply lower, down 12.6% in four trading days. The bottom on April 8th marked a 20% decline in the S&P 500, constituting the fifth bear market since 2000.

After significant unease in the bond market, Trump softened his tone, announcing a 90-day pause on tariff implementation. This caused a rapid reversal in market prices. By the end of April, markets recovered their losses from the beginning of the month. By the end of the quarter, US stocks were hitting new all-time highs.

The bull market in Risk assets came despite what some would consider a series of pessimistic news. Israel launched a surprise attack on Iran, targeting military and nuclear facilities. The brief war sent oil prices higher but did little to equity markets. Domestically, the Federal Reserve met and voiced concerns over inflation, ultimately deciding not to cut interest rates.

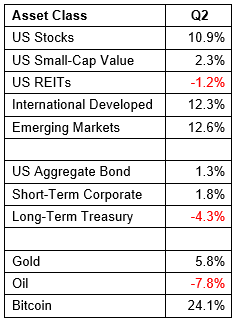

Price Action

While the bounce back in U.S. Stocks drew the headlines, international stocks edged out domestic equities to build on their strong year.

Within U.S. stocks, technology led the way with Nvidia gaining 46% to become the most valuable company in the world. Communication services and industrials (buoyed by defense spending) also fared well, while energy and healthcare finished Q2 in negative territory.

Emerging Markets also did well in the second quarter despite China struggling with both its domestic economy and receiving unwanted attention on the tariff front.

Short and intermediate-term Bonds posted solid returns for the quarter, while long-dated bonds sold off as long-term interest rates rose.

- While U.S. Large-Cap stocks recovered well (11%), U.S. Small-Cap Value stocks only gained 2% for the quarter. Small-Cap Value is just about the only part of the market trading below historical valuations.

- REITs again proved to be uncorrelated with the broader U.S. market, falling 1.2% despite the strong rally in equities.

- International stocks rose more than 12%, bringing their yearly total to 19%.

- The aggregate bond market gained a little more than 1% for the quarter, but long-dated treasuries declined by 4%

- Speculators in cryptocurrency were rewarded with a stellar quarter as Bitcoin gained 24%, reaching new all-time highs

- Housing prices reversed their recent poor fortunes, gaining 1.8% for the last 3 months we have data.

Looking Forward

Tariff policy will likely be the biggest driver of markets in Q3. The 90-day pause expired on July 9th, but it’s unclear to what extent higher tariffs will be enacted. Tariff revenue was up in Q2, roughly 4x from where it was a year ago (going from $6 billion a month to $26 billion). Annualized at $300 billion, that represents 1% of U.S. Gross Domestic Product.

Beyond that, Republicans passed a tax and spending bill that which the market seemed to take as good news. It is expected to add $4 trillion to the national debt in the coming decade, increasing our anticipated debt growth from $20 trillion to $24 trillion. This more than anything helps explain the rise in long-term treasury yields.

Geopolitical news is difficult to anticipate, but it seems action in Ukraine and the Middle East is being treated as a non-event for markets and it would be surprising to see that change.

Data around tariff impact on inflation could pose a headwind for markets especially given the stretched valuations seen in U.S. Stocks. The S&P 500 is trading at 22x forward earnings, which is rather high by historical standards. Hopefully our economy will see growth to justify current prices.