Q1 2026 Market Commentary

BY ETHAN GILBERT, CFA, CFP, PARTNER

The first two months of the quarter saw stocks and bonds broadly appreciating as markets focused on the long-term economic impacts of artificial intelligence and anticipated moves by the Federal Reserve. Up until this point, AI tailwinds had been uplifting technology stocks, but the bullish outlook turned as some began to fear tech companies would be the first to be replaced by AI. This led to a selloff in software companies as well as financial stocks that had facilitated “private credit” loans to small software companies.

The first two months were quickly forgotten as the U.S. and Israel attacked Iran on February 28. News surrounding the war became the only factor affecting markets, with the primary driver being the price of oil. With 20% of the world’s oil shipping through the Strait of Hormuz each day, its closure has had a tremendous impact on the price of this inelastic good. As oil prices increased 80%, fears of prolonged inflation began weighing heavily on all markets.

Price Action

The first two months of the year saw a rotation out of U.S. large-cap technology stocks and into just about everything else. While U.S. tech stocks were flat, small-cap stocks, REITs, and international stocks were all up 10%. A modest decline in interest rates has pushed bonds up 1.5% and gold rallied 23%.

March saw a sharp contrast as the conflict with Iran turned everything on its head. Everything not named oil sold off, with stocks dropping roughly 10% across the board. Interest rates rose 0.3%, causing bonds to give back all their gains from the first two months, finishing the quarter flat.

Gold declined 15% in March, despite the war creating perfect conditions for a rally. The precious metal is thought of as a safe haven in times of geopolitical uncertainty and one of the best hedges against inflation. I have yet to read a compelling explanation for this movement.

Stocks saw an unusual decline in correlation this quarter, with winners and losers that would have been hard to predict even if you knew the news beforehand. The technology sector declined 9%, dragged down by stocks like Microsoft (-23%) and Intuit/Turbo Tax (-35%); however, Intel and Micron were up 19% each. Industrials gained 4%, with Lockheed Martin up 26%, but GE Aerospace and Defense fell 8%. Energy stocks gained 38%, but financials, another staple of value funds, declined 9%.

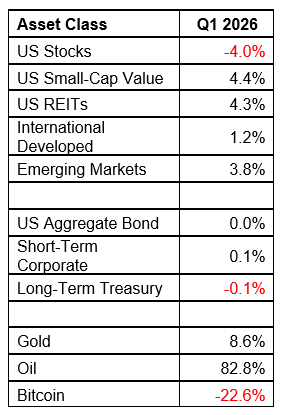

- US stocks hit new highs midway through the quarter but ended up declining 4% by the end of March.

- Despite the war with Iran harming foreign stocks the most, international developed stocks finished Q1 up 1% and emerging markets were up 4%.

- U.S. small-cap value stocks and REITs both finished the quarter up 4%.

- Across the board, bonds finished flat as the interest they paid was offset by rising rates. The good news is that their yield going forward is higher.

- Commodities did well, with oil gaining 80% as the conflict sent prices markedly higher.

- Speculators in Bitcoin were again frustrated in Q1 (-23%), causing some to question how effective of an inflation hedge cryptocurrencies really are.

- The housing market continued to soften, falling 0.5% for the last three months for which we have data. Rising mortgage rates could continue to harm home prices

Looking Forward

Markets in the last month were driven by the price of oil and that is being dictated by the conflict in the Middle East. As long as the conflict continues, prices should remain elevated and we can expect worsening stock and bond prices. But when a resolution finally happens most expect a strong rally in markets.

At the beginning of the year, the Federal Reserve was expected to cut rates twice. Now with higher energy prices, economists have increased their expectations for inflation, and subsequently, the market is no longer pricing in ANY rate cuts in 2026. However, complicating forecasts is the expected appointment of Kevin Warsh as the new Fed chair in May. It’s hard to anticipate how hard he will push for lower rates and if he does, how successful he will be.

Most clients, from listening to the doom and gloom of the news, assume their accounts are faring much worse than they really are. Our average client account was down about 1% for the quarter. This is another testament to diversification and maintaining a steady perspective through turbulent times. Much research has shown that investors who develop a sound plan, and stick to it, achieve great results.